The Optimal Order For Investing Your Money (2025)

In the ever-evolving landscape of personal finance, knowing the optimal order for investing your money is more critical than ever. With a plethora of investment options available and an increasing number of individuals seeking financial independence, understanding where to allocate your resources first can significantly impact your financial future. In this comprehensive guide, we'll explore the optimal order for investing your money in 2025, considering current market trends, economic factors, and personal financial goals. We'll delve into the rationale behind each step, providing detailed insights to help you make informed decisions.

Step 1: Build an Emergency Fund

Before diving into the world of investments, it's crucial to establish a solid financial foundation. An emergency fund acts as a financial safety net, providing liquidity during unexpected events such as medical emergencies, job loss, or urgent repairs. Ideally, your emergency fund should cover three to six months' worth of living expenses.

In 2025, the importance of an emergency fund cannot be overstated. Economic uncertainties, inflationary pressures, and job market fluctuations make having accessible cash reserves essential. Keeping your emergency fund in a high-yield savings account or a money market account ensures liquidity while earning a modest return. This step provides peace of mind and prevents you from dipping into your investments during financial crises.

Step 2: Pay Off High-Interest Debt

High-interest debt, particularly credit card debt, can be a significant barrier to financial growth. The interest rates on such debts often exceed the returns on most investments, making it a priority to pay them off as quickly as possible. By eliminating high-interest debt, you free up more money for future investments and reduce financial stress.

In 2025, interest rates are expected to remain relatively high due to global economic trends. Therefore, focusing on debt repayment can provide a guaranteed return equivalent to the interest rate of the debt. Once high-interest debt is under control, you can allocate funds towards more lucrative investment opportunities.

Step 3: Contribute to Your Employer's 401(k) Plan (Up to the Match)

If your employer offers a 401(k) plan with a matching contribution, it's wise to take full advantage of this benefit. Employer matching is essentially free money added to your retirement savings, making it one of the most advantageous investment steps.

In 2025, with the continued emphasis on retirement planning, contributing to your 401(k) up to the employer match is a no-brainer. The tax advantages, such as deferred taxation on contributions and earnings, enhance the appeal of this investment. Additionally, automatic payroll deductions make it easier to consistently contribute without the temptation to spend.

Step 4: Pay Off Moderate-Interest Debt

After securing your emergency fund and taking advantage of employer matching, the next step is to tackle moderate-interest debt. This includes debts with interest rates lower than credit cards but higher than mortgage rates, such as personal loans or auto loans.

Paying off moderate-interest debt in 2025 remains a sound strategy as it frees up cash flow and reduces financial obligations. The goal is to create a balance between debt repayment and investment growth. By eliminating these debts, you can focus on building wealth through various investment avenues without the burden of monthly debt payments.

Step 5: Max Out an Individual Retirement Account (IRA)

Once you've addressed high-interest and moderate-interest debts, it's time to maximize your contributions to an Individual Retirement Account (IRA). Both Traditional and Roth IRAs offer tax advantages that can significantly enhance your retirement savings.

In 2025, the contribution limits for IRAs are expected to increase, allowing for greater tax-advantaged savings. A Traditional IRA provides tax-deductible contributions, reducing your taxable income in the present, while a Roth IRA offers tax-free withdrawals in retirement. Depending on your current tax bracket and retirement goals, either option can be highly beneficial. Maximizing IRA contributions helps diversify your retirement portfolio and ensures a more secure financial future.

Step 6: Build a Health Savings Account (HSA)

If you have a high-deductible health plan (HDHP), contributing to a Health Savings Account (HSA) is a wise investment choice. HSAs offer triple tax advantages: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are also tax-free.

In 2025, healthcare costs are projected to continue rising, making an HSA an essential tool for managing future medical expenses. Additionally, HSAs can serve as a supplemental retirement account, as funds can be used for non-medical expenses after age 65 without penalties (though they will be subject to income tax). By investing in an HSA, you not only prepare for healthcare costs but also add another layer to your retirement planning.

Step 7: Max Out Your 401(k) Contributions

After taking advantage of your employer's match and other tax-advantaged accounts, the next step is to maximize your 401(k) contributions. The annual contribution limits for 401(k) plans are higher than those for IRAs, allowing you to save more for retirement in a tax-advantaged manner.

In 2025, with the growing emphasis on retirement readiness, fully funding your 401(k) is a strategic move. The compounding effect of tax-deferred growth can significantly enhance your retirement savings over time. Additionally, many 401(k) plans offer a variety of investment options, allowing you to diversify your portfolio according to your risk tolerance and financial goals.

Step 8: Invest in a Taxable Brokerage Account

Once you've maxed out tax-advantaged retirement accounts, it's time to consider investing in a taxable brokerage account. These accounts offer greater flexibility, allowing you to invest in a wide range of assets, including stocks, bonds, mutual funds, and ETFs.

In 2025, taxable brokerage accounts remain a crucial component of a well-rounded investment strategy. While they lack the tax advantages of retirement accounts, they provide liquidity and the ability to access funds without penalties. Additionally, capital gains and dividends can be strategically managed to optimize tax efficiency. Investing in a taxable account allows you to pursue financial goals beyond retirement, such as buying a home, funding education, or achieving financial independence.

Step 9: Explore Real Estate Investments

Real estate has long been a popular investment option, offering potential for steady income and capital appreciation. Investing in real estate can take various forms, including purchasing rental properties, investing in real estate investment trusts (REITs), or participating in real estate crowdfunding platforms.

In 2025, the real estate market continues to offer opportunities for diversification and wealth building. Low interest rates and growing demand for rental properties make real estate an attractive investment. Additionally, real estate provides a hedge against inflation, as property values and rental income tend to rise over time. However, it's essential to conduct thorough research and consider factors such as location, market trends, and property management before investing in real estate.

Step 10: Invest in Alternative Assets

Alternative assets, such as commodities, cryptocurrencies, and private equity, can add diversification to your investment portfolio. These assets often have low correlation with traditional investments, providing potential for enhanced returns and reduced risk.

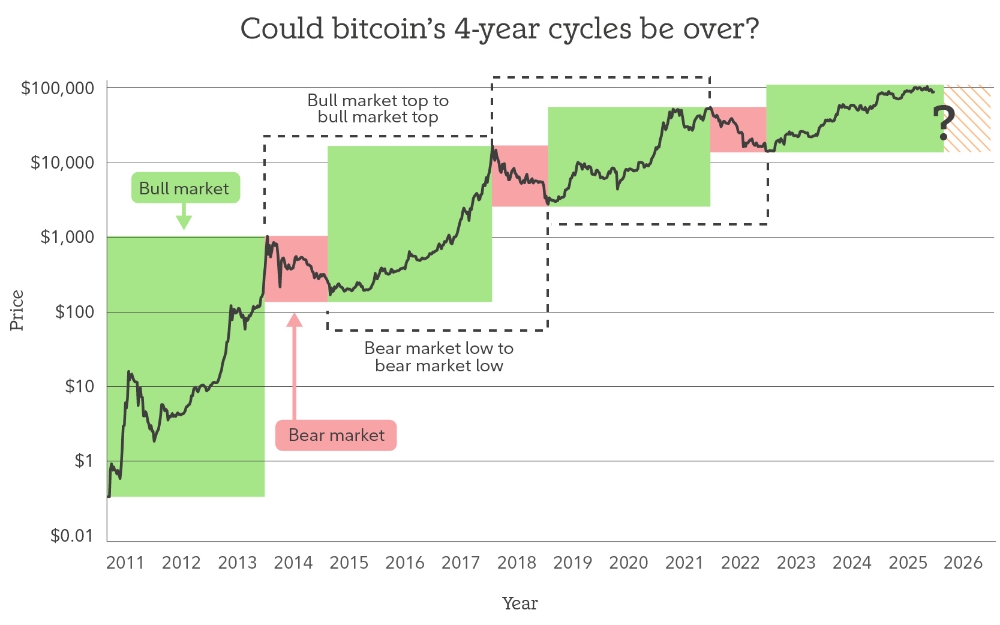

In 2025, the growing acceptance of alternative assets makes them an intriguing option for investors seeking to diversify their portfolios. Cryptocurrencies, in particular, have gained traction as a hedge against inflation and economic instability. However, it's important to approach alternative investments with caution, as they can be highly volatile and require a deep understanding of the market. Allocating a small portion of your portfolio to alternative assets can provide growth potential while mitigating overall portfolio risk.

Step 11: Continuously Reevaluate and Rebalance Your Portfolio

The final step in the optimal order of investing is to continuously reevaluate and rebalance your portfolio. Investment goals, risk tolerance, and market conditions can change over time, necessitating periodic adjustments to your portfolio.

In 2025, staying proactive and adaptable is key to successful investing. Regularly reviewing your portfolio ensures that it remains aligned with your financial objectives. Rebalancing involves adjusting the allocation of assets to maintain the desired risk level and maximize returns. Additionally, staying informed about market trends and economic developments can help you make informed investment decisions and seize new opportunities.

Conclusion

Investing your money in the optimal order is crucial for achieving financial success and security. By following the steps outlined in this guide, you can build a solid financial foundation, maximize tax-advantaged savings, and strategically allocate resources to achieve your financial goals. From establishing an emergency fund to exploring alternative assets, each step plays a vital role in creating a well-rounded investment strategy.

In 2025, the investment landscape continues to evolve, presenting both opportunities and challenges. By staying informed, disciplined, and proactive, you can navigate the complexities of investing and build a prosperous financial future. Remember, the key to successful investing lies in understanding your financial goals, risk tolerance, and the ever-changing market dynamics. With careful planning and execution, you can optimize your investment journey and achieve long-term financial success.

You May LIKE :

Why Everyone SEEMS to Have More Money Than You

12 Things I'm NOT Buying In 2025

11 Essential Financial Goals To Achieve Before 30