Liquid Staking Derivatives on Ethereum

Tokenizing ETH yield

Introduction

Even if you got interested in DeFi this year, you certainly have heard about liquid staking. Though it may sound cryptic, liquid staking is just one form of regular staking where users delegate their tokens to a validator node on a Proof-of-Staking (PoS) blockchain network. With regular staking, you cannot withdraw your assets from the pool once they are locked up. The problem should be obvious: If there are other opportunities to earn more yield, you are not able to exploit them. So, you have an opportunity cost. You have market risk as well; if the price plunges before your crypto is unlocked, the value of your holdings will go down which easily can outweigh the yield you received from staking.

Liquid staking was offered as a solution to fix these problems. For depositing their crypto into a staking pool via a third-party liquid staking provider, users receive derivative tokens the value of which comes from the price of the underlying digital asset. In the case of ETH, the largest altcoin and around which the biggest LSD (liquid staking derivatives) market has been built, the value of LSDs is pegged to the ETH price.

Liquid staked tokens

First, let’s define what a liquid staking derivative (LSD) is. In finance, traditional or decentralized, a derivative indicates a security deriving (that is where the term “derivative” comes) its value from an underlying asset. An option on Apple stock or BTC futures are derivatives because the prices of both the option and the futures contracts depend on the price of Apple share and Bitcoin respectively. In the context of blockchain networks, LSD is just a digital asset representing a token staked into a DeFi protocol. Even if you stake your stake your tokens within a protocol, you can use LSDs on other decentralized applications.

For the Ethereum blockchain LSDs were a popular product up to Shapella upgrade. While ETH holders locked their Ether holdings to secure the blockchain, LSDs gave them flexibility to utilize their tokens elsewhere if they wished to do so. The Shapella upgrade unlocked a great amount of ETH which increased the need for liquid Ether staking protocols. At the time pf writing, more than $18 billion is deposited into LSD protocols with their TVL surpassing even that of DEXes. Liquid staking is beneficial not only for users but for the whole DeFi as well. It is believed that over time it will result in more decentralization because it lowers the barriers of entry. An increase in the number of validators will create a more robust and secure PoS network. On the Ethereum network, for example, if you want to be a validator, you have to invest at least 32 ETH which is a huge sum for the majority of retail users. Liquid staking makes it possible for users to contribute to the decentralization, stability, and security of the blockchain network with the amount much less than 32 ETH, and to earn yield in exchange for locking up their tokens.

Liquid staking is beneficial not only for users but for the whole DeFi as well. It is believed that over time it will result in more decentralization because it lowers the barriers of entry. An increase in the number of validators will create a more robust and secure PoS network. On the Ethereum network, for example, if you want to be a validator, you have to invest at least 32 ETH which is a huge sum for the majority of retail users. Liquid staking makes it possible for users to contribute to the decentralization, stability, and security of the blockchain network with the amount much less than 32 ETH, and to earn yield in exchange for locking up their tokens.

ETH Liquid Staking

The liquid staked ETH market is huge. It has grown even more since Shapella upgrade on April 12. The number of locked ETH coins increased by 4.4 million bringing the total number to 22.58 million. The main reason for the demand probably comes from large ETH holders who prefer to stake their coins instead of passively owning them. Given that deflationary forces may cause ETH price to surge, it is relatively safe to assert that this trend will continue.

The market is not without problems though. There are risks associated with other DeFi sectors:

- Smart contract risk which is inherent to almost all DeFi sectors / protocols / apps.

- Counterparty risks should not be ignored either; there’s always a chance that a third-party liquid staking service provider won’t fulfill his obligations.

- You have to consider regulatory risk as well. With the recent war of SEC against the largest centralized exchanges (CEX) and their staking services, it is not unlikely that one day SEC will come after the liquid staking solutions.

- Depeg risk. it may be a strong statement, but I’ll say it anyway. Whenever you hear “derivative” in DeFi, you have to assume the depeg risk, that is the price of the derivative asset will deviate from the price of the underlying asset. Since LSD tokens are traded on the secondary market, occasionally their prices can fall below the peg; this was the case in 2022 June in the aftermath of Terra blockchain collapse when stETH/ETH was trading at 0.93. This was due to a popular recursive borrowing stETH strategy. Aave adding stETH as a collateral in 2022 February made the strategy possible — deposit stETH as collateral, borrow ETH against your collateral, and buy more stETH with ETH. When there was strong market liquidity and relatively less volatility in the markets, depeg stETH/ETH worked well. But liquidity crunch several months later sent the peg below parity. This is detrimental not only to one protocol and its liquidity providers, but also to the liquid staked ETH market. When the derivative asset experiences a significant depeg, users tend to withdraw their funds which leads to liquidity crunch and may impact all LSD protocols.

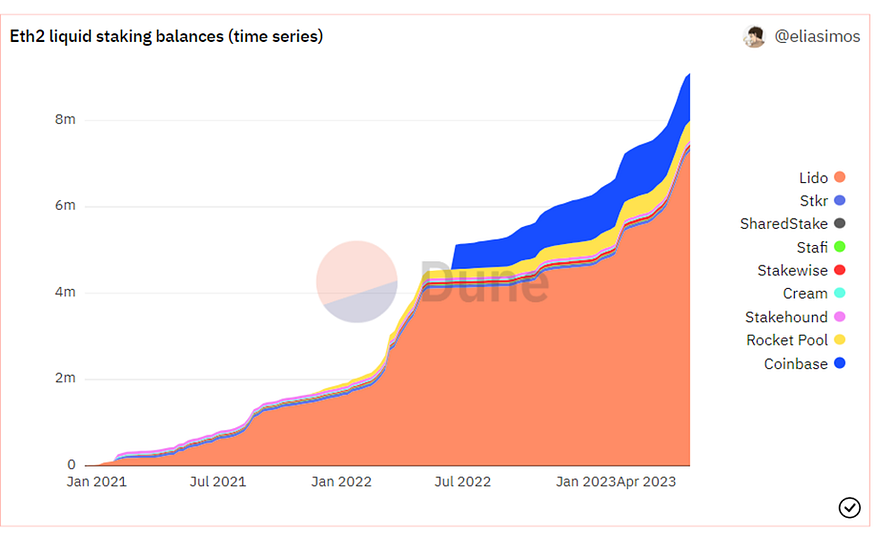

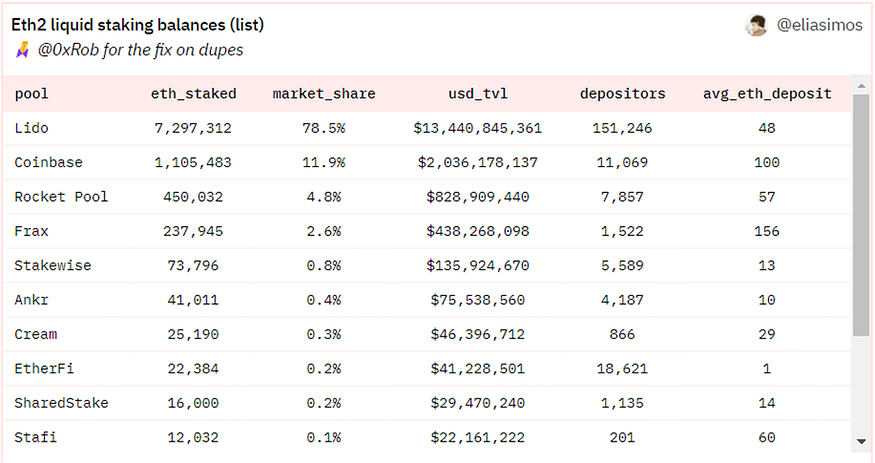

However, the most important issue with the current market is centralization. The biggest player in the field is Lido in which hands concentrated about 90% of liquid staked Ether. If we exclude Coinbase, which is a centralized exchange and thus should not be considered DeFi, Lido seems the only significant player in the Liquid Staked Ethereum market. At the time of writing, it has 16 times more ETH locked than the second-largest protocol, Rocket Pool has. Not only for the TVL (Total Value Locked) but also for the number of depositors Lido is the market leader as the chart below shows:

Not only for the TVL (Total Value Locked) but also for the number of depositors Lido is the market leader as the chart below shows: But here is the problem. If some sector of the market is dominated by one actor, then this is not true decentralized finance. Depeg from ETH price or a critical smart contract bug would severely affect the LST (liquid staked token) market. There’s also regulatory risk — sanctions or charges by regulatory bodies can disrupt the system regardless of how big it is at the moment. The stakes (pun intended) are just too high to remain LST market centralized in the hands of one big actor.

But here is the problem. If some sector of the market is dominated by one actor, then this is not true decentralized finance. Depeg from ETH price or a critical smart contract bug would severely affect the LST (liquid staked token) market. There’s also regulatory risk — sanctions or charges by regulatory bodies can disrupt the system regardless of how big it is at the moment. The stakes (pun intended) are just too high to remain LST market centralized in the hands of one big actor.

Protocols

Asymmetry Finance

The emerging concept in the field of LSDfi is an LSD basket. There are many LSD projects, and we believe many more liquid staking solutions will be built for blockchain networks, especially for Ethereum where most of the capital is locked in. It is and will become more difficult for retail investors to choose which protocol to deposit her Ether into. Protocols building LSD baskets combine tokens of several of these liquid staking projects into one product. This mitigates risk and makes LSD investing more user-friendly. Index Coop, the largest provider of on-chain structured crypto products and DeFi indices, has designed two products, namely gtcETH and dsETH which are index tokens of leading Ethereum liquid staking projects.

Asymmetry Finance attempts to fix the problem by bringing decentralization to the staked Ether market. They are building Asymmetry Ethereum Indices which are DeFi native index products. Indices are built upon LST products. The protocol has two products at the time of writing — afETH and safETH. You can think of these products as exchange-traded funds (ETF). As ETFs, the performance of these LST products also depend on the underlying primitive items, in this case tokens of the staked ETH providers.

safETH

Simple Asymmetry Finance Ethereum, or safETH is built with institutional investors in mind. Those with large ETH holdings want to avoid exposure to centralized protocols. safETH is designed to offer a more decentralized way to get ETH exposure while simplifying the process for users. The way safETH works is as follows. Once you deposit ETH you can mint safETH. Behind the scenes, your ETH deposit is allocated to the following Liquid Staking Derivatives:

- wstETH from Lido Finance. As already mentioned, Lido Finance is the largest staked ETH provider with more than 5 million Ether locked at the moment.

- rETH from RocketPool. With more than 450,000 ETH staked, RocketPool is the second largest protocol in the staked Ether market.

- sfrxETH from Frax Finance. Launched in October 2022, Frax Finance has is a rapidly growing protocol containing about 230,000 staked ETH.

The following two staking protocols will be added to the safETH basket once audit process is completed:

- sETH2 from Stakewise. Stakewise is another liquid staking protocol with nearly 74,000 ETH.

- ankrETH from Ankr. It is the oldest protocol in this market with nearly 40,000 staked ETH.

At the time of writing, all underlying products have equal weights. The Whitepaper of Asymmetry Finance mentions that weights of safETH products are set at:

- stETH — 14%

- rETH — 20%

- frxETH — 29%

- sETH2–20%

- ankrETH — 17%

But this is subject to change since the protocol will allow Asymmetry DAO to decide weights of different staking protocols. With the addition of more products the composition of safETH, and their weights will change. More products will bring more diversification and less dependency on any single liquid staked ETH protocol.

Deviation from the peg One risk to hold your ETH in one staking protocol is the depeg risk, that is the risk of the deviation of the protocol’s staking ETH token’s price from ETH price. The chart and the table display the deviation of various liquid staked ETH tokens from ETH. I think depositing into safETH will significantly mitigate the depeg risk because it is built upon several other tokens. The price of safETH reflects the value of the basket of underlying digital assets. Even if one of the underlying tokens deviates from the peg, there’s a chance that other tokens will exhibit a more stable peg to the ETH price. However, it is much more difficult to speculate on how safETH will behave during the wild market swings.; but even in that case I believe it is much safer to put your money in an ETF-like product, such as safETH rather than in a single staking derivative token.

One risk to hold your ETH in one staking protocol is the depeg risk, that is the risk of the deviation of the protocol’s staking ETH token’s price from ETH price. The chart and the table display the deviation of various liquid staked ETH tokens from ETH. I think depositing into safETH will significantly mitigate the depeg risk because it is built upon several other tokens. The price of safETH reflects the value of the basket of underlying digital assets. Even if one of the underlying tokens deviates from the peg, there’s a chance that other tokens will exhibit a more stable peg to the ETH price. However, it is much more difficult to speculate on how safETH will behave during the wild market swings.; but even in that case I believe it is much safer to put your money in an ETF-like product, such as safETH rather than in a single staking derivative token.

Lybra Finance

LSDfi may become the hottest topic of upcoming months. The market of staked ETH is around $17 billion. Holders of that huge capital will seek smart ways to increase yield on their Ether holdings which otherwise would sit idly in their wallets. LSDs are perhaps the best (in terms of most flexible) way to do this. Considering that TVL of emerging LSDfi projects is less than half billion at the time of writing, there is a lot of room for the market growth. That is why we think that 2023 summer might be “LSDfi summer” like 2020 summer was DeFi summer.

Lybra Finance is one of the recent LSDfi protocols gaining traction. Its TVL surged almost 1,000% within two weeks after the launch. The main component of the protocol is eUSD, a yield-bearing stablecoin which can be borrowed if a user deposits ETH or stETH, which is, as you recall, Lido Staked ETH. Though the collateral ratio is 170%, Lybra doesn’t charge fees or interest for minting or borrowing eUSD. Users can hold the stablecoin in which case they will earn interest, or they can purchase even more Ether with their eUSD which is essentially a levered long position in ETH.

Asymetrix

Asymetrix seeks to make something as boring as ETH staking more interesting and fun. It is a no-loss lottery where you cannot lose your invested capital but can win big. Users deposit stETH in a pot, and rewards from staked Ether are distributed to random winners on a weekly basis. But here is the thing. Though the reward is random through the use of Chainlink’s VRF (Verifiable Random Function), the outcomes are not. Your odds depend on the amount deposited into the lottery, and on how long you have deposited ETH, i.e., on the duration. Aside from the opportunity cost of earning yield on the staked ETH, there is no downside in participating in Asymetrix lottery. That is a protocol for true ETH degens!

Pendle

Some novel protocols, namely Flashstake and Pendle allow users to trade their future yield. What they do is give the users flexibility over their yields; that is, you can receive your interest upfront if you choose to do so.

When you supply liquidity into a yield derivative protocol, your assets are deposited into yield-generating protocols which give you back yield-bearing tokens. These tokens then are separated or tokenized into two assets: principal tokens and yield tokens. Different protocols can name them a bit differently, but the idea is the same across DeFi. You can think of the principal tokens as the amount of your assets because they are; they represent the amount of deposited assets. Future yield from the underlying assets is indicated by the yield tokens.

Extracting yield from principal tokens (PT) allows a user to buy an underlying asset at a discount price. It works like zero-coupon bonds in traditional finance. Since zero-coupon bonds don’t pay any interest, i.e., they don’t have coupon payments, they tend to trade at a discount to their face value. Which means you can buy a $1,000 bond for $990 if there’s a 1% discount. It works exactly the same way here. Let’s say, on Pendle you can buy ETH for 3% discount with 6 months’ maturity. What this means is that you can buy 50 ETH by paying only 48.5 ETH. Six months later you are entitled to claim the full amount, 50 ETH. The thing is that you can still sell your ETH before the maturity of PT in exchange for an amount which will likely be higher than what you have paid but not full 50 ETH. That is how you can control your future yield.

Yield tokens (YT) allow users to earn yield from the underlying asset after the expiry date. You can buy YT at an implied annual percentage yield (APY) if you believe that the yield on the underlying asset will rise. If the APY is higher than the original implied APY at which you’ve purchased, you’ll make profit; otherwise, you’ll lose money at the redemption of YT.

Conclusion

Liquid staking ETH market is big with nearly$20 billion TVL. But the market is extremely concentrated with nearly 30% of staked Ether locked in one protocol, namely Lido. Now, we don’t hold anything against Lido Finance; they pioneered the market, paved the way for its further progress, and have built a great product. But it isn’t unreasonable to claim that the current state of the market is against the nature of Ethereum, and of decentralized finance in general.

![[ℕ𝕖𝕧𝕖𝕣] 𝕊𝕖𝕝𝕝 𝕐𝕠𝕦𝕣 𝔹𝕚𝕥𝕔𝕠𝕚𝕟 - OM(G) , My Biggest Bag Was A Scam????](https://cdn.bulbapp.io/frontend/images/99de9393-38a8-4e51-a7ab-a2b2c28785bd/1)